Global Broadband Subscribers in Q2 2025: 5G FWA, satellite and FTTP thrive, while Spain says goodbye to copper

- Jolanta Stanke

- Oct 17, 2025

- 9 min read

Summary

This report provides analysis of trends in global and regional broadband subscriptions, technology adoption, and growth rates in various markets in Q2 2025.

Global broadband subscribers surpassed 1.53 billion in Q2 2025, marking a 1.1% growth. Broadband subscriptions[1] declined in 24 countries[2], compared to 22 in Q1 2025. In some of these markets consumers are migrating to mobile broadband, others are experiencing economic headwinds or are already highly saturated. Some are still in the midst of conflict. Globally, the growth in Q2 2025 has increased slightly, compared to the same quarter of 2024.

Other key points:

In terms of growth, India remained at the top of the largest 20 fixed broadband markets with a 6.7% quarterly growth rate.

The share of FTTH/B in the total fixed broadband subscriptions increased further and stood at 72.68%. Broadband connections based on other technologies saw their market shares shrink again, with an exception of satellite and fixed wireless access (FWA).

Year-on-year, FTTH/B connections grew by 7.2%. Satellite and FWA saw an even higher annual growth (41.6% and 31% respectively).

Legacy copper subscriptions declined by 12.1% y-o-y, while FTTx lines (mainly VDSL) went down by 6%, with Spain becoming one of the first countries in the world and the first major European economy to shut down its copper network completely.

5G FWA take-up accelerated, especially in India and the US, as a result of aggressive investments by Reliance, Bharti Airtel, T-Mobile, Verizon and AT&T.

[1] Whenever we refer to ‘broadband’ in this report, we mean fixed broadband. Also, ‘subscriptions’ and ‘connections’ are used interchangeably.

[2] It is possible there will be restatements in the coming quarter/s and single period data should be viewed in that light. Decline in some markets can be due to changes in methodology used by national regulatory authorities.

Global and regional trends in broadband subscriber growth

In Q2 2025, the global fixed broadband subscriber figure grew by 1.1%, exceeding 1.53 billion. In line with seasonal trends, the growth rate was slower than in the previous quarter but it was slightly higher than in the respective quarter of 2024 (Figure 1 and Table 1).

Table 1. Global broadband subscribers and quarterly growth rates. Source – Point Topic.

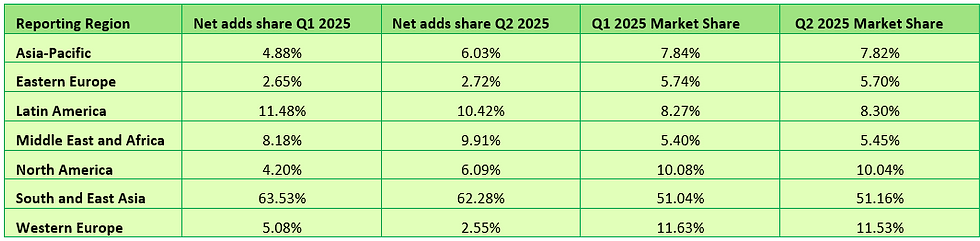

South and East Asia continues to claim the largest share of net adds in global fixed broadband subscribers, though it dropped slightly quarter-on-quarter from 63.5% to 62.3%. This was largely due to the slower quarterly growth in China, the largest broadband market of the region[3], which is inevitable due to the increasing market saturation (Table 2 and Figure 2).

[3] Although we use them in our reports, we cannot vouch for the country’s officially reported broadband subscriber figures which suggest household penetration well over 100%.

Table 2. Share of fixed broadband subscribers and trends in net adds by region. Source – Point Topic.

Other regions saw their net adds shares expand, with an exception of Latin America and Western Europe. In Western Europe, whose net adds share halved, most of the Scandinavian countries, the UK and some others saw a decline in fixed broadband subscribers, as the extent of migration to gigabit capable technologies was not sufficient to offset the decline in copper based subscriptions.

In this context, Spain became one of the first countries to officially shut down its copper network. The Spanish incumbent Telefonica switched off its last copper exchanges in May 2025, and the country no longer has ADSL or VDSL connections. Nevertheless, with 90% of its broadband subscribers on FTTH, Spain reported a healthy 1.1% quarterly growth in total fixed broadband connections. The country has a near-universal FTTH coverage.

North America saw a particularly large increase in the net adds share (6.1% this quarter compared to 4.2% in Q1 2025), as the quarterly growth in Canada recovered, following a previous dip due to the ‘clean-up’ of subscriber statistics by various operators.

Broadband penetration among population is one of the factors affecting growth rates, as illustrated by the Middle East and Africa, which remains at the bottom right corner of the penetration – growth chart (Figure 3), signifying the lowest penetration (9%) and the highest quarterly growth rate (2%). It retains a good growth potential, especially for FWA and satellite broadband connections. Some countries in the region are also heavily investing in FTTP.

South and East Asia, Latin America and Asia-Pacific occupy the middle ground in terms of broadband penetration but the former two regions experienced higher quarterly growth (1.3% and 1.4%) compared to Asia-Pacific (0.8%). For example, in Latin America, the large markets of Mexico, Peru and Ecuador recorded a higher than 2% quarterly growth.

Western Europe and North America are in the top left corner of the chart, with high penetration accompanied by modest growth and a decline in some markets, e.g. in Scandinavia and the UK. Eastern Europe also saw a relatively sluggish growth, whether it’s due to already high penetration in some markets or economic challenges.

Diminishing growth potential in some countries continues to lead to mergers and acquisitions. In May 2025, AT&T in the US agreed to acquire substantially all of Lumen’s Mass Markets fibre broadband business which totals about 1 million fibre customers and reaches more than 4 million fibre locations (effectively, premises passed) across 11 states. The deal intensified competition for cable incumbents (Comcast, Charter, Altice) and regional fibre ISPs. (In several of the markets involved, there are overlapping cable / hybrid networks).

Country and technology trends in broadband subscriber growth

In Q2 2025, we registered the highest broadband subscriber growth rates mainly in the least saturated broadband markets of Middle East and Africa, and Latin America, often from a relatively low base (Figure 4). The sizeable markets of India, the Philippines and Viet Nam also continued to grow at a healthy pace.

In the Philippines, the growth was primarily driven by investment in the full fibre infrastructure. Globe, one of the three largest market players, expanded fibre coverage to 600 towns across the Philippines in mid-2025. The shift in Globe’s revenue mix toward fibre (almost 90%) suggests that more customers are migrating from legacy technologies or new customers are opting for fibre. At the governmental level, the Second Digital Transformation Development Policy Loan, approved in November 2024, seeks to reduce barriers to entry and competition in the broadband sector. These efforts are expected to narrow the digital divide by reducing the cost of internet and expanding digital services and opportunities to over 20 million Filipinos.

Vietnam’s government also adopted a programme to encourage private sector investment in digital infrastructure, including high-quality broadband connectivity. As a result, operators providing fixed broadband services are expected to achieve an average annual revenue growth of 10–12 percent.

Looking at the largest twenty broadband markets, once again all except the UK saw fixed broadband subscriber growth in Q2 2025 (Figure 5). The UK saw a -0.05% decline (compared to -0.3% in the previous quarter), as the FTTP growth was not sufficient to offset the decline in DSL, FTTx and cable broadband connections. For several quarters now India is at the top of this cohort, with a 6.7% growth, continuing to show huge growth potential due to the low fixed broadband penetration (16% of households) and the fast growing economy. Along with Canada, India also saw the largest increase in quarterly growth, compared to Q1 2025.

In India, the growth was driven by a further dramatic increase in 5G FWA connections (+21% quarter-on-quarter), with fibre broadband subscriptions also growing at a healthy pace. In many underserved and remote areas, FWA offers a more scalable and faster deployment alternative to fibre or copper. At the same time, Indian telecom operators are expanding FTTP more aggressively, especially in urban areas, to meet demand for high-speed symmetrical services. The launch of National Broadband Mission 2.0 (2025–2030) signals Indian government’s commitment to expanding broadband access and improving quality.

Technology trends

The market share of fibre based broadband subscriptions (FTTH/B) has expanded further – quarter-on-quarter it went up by 0.32% and stood at 72.68%. Broadband connections based on cable, copper and FTTx technologies saw their market shares shrink further. Satellite and wireless (FWA) broadband connections expanded their market shares to 0.5% and 2.8% respectively.

Table 3. Changes in broadband technology market shares. Source – Point Topic.

Among the markets with at least 0.5 million fibre broadband connections, we recorded the highest FTTH/B growth rates in Egypt (15.2%), South Africa (12.3%), Algeria (12.3%) and Greece (12.1%) (Figure 6). This ranking once again contains mature broadband markets of Greece, Belgium and the UK. These countries were relatively late in focusing on fibre as the main broadband technology, with the incumbents initially betting on VDSL. Partly because fibre networks there are relatively new, these markets are in the bottom ten by FTTH/B take-up rates among the European countries. (See our piece on FTTP take-up in Europe).

Globally, healthy quarterly FTTH/B growth rates were spread around the world, with the less advanced economies and more youthful fibre markets generally exhibiting higher growth (Figure 7).

In 12 months to the end of Q2 2025, the number of DSL lines saw another decline (-12.1%), while FTTH/B connections grew by 7.2%. The decline in FTTx was -6%, while cable (HFC) broadband subscribers dropped by -0.9% (Figure 8).

The decline in copper and FTTx (mainly VDSL) is not surprising. When it comes to cable/HFC, it is not immune to competition from other technologies either. The US is a good example, being the largest cable market globally. There the decline has continued as major players such as Comcast, Charter, Cox, Altice and others are losing customers. Competition from telcos who are rapidly expanding their fibre footprints (AT&T, Verizon, Frontier, Lumen, Consolidated Communications) and offering symmetric bandwidth, superior upload speeds and lower latency is partly to blame. At the same time, cable broadband prices have risen steadily due to promotional offer expirations, ‘network fees’, and equipment costs. Finally, 5G FWA home broadband from T-Mobile, Verizon and AT&T has exploded, with their customer numbers jumping year-on-year by 31%, 34% and 194% respectively.

Globally, wireless broadband (FWA, 5G FWA and LTE fixed) connections also continued to grow – they went up by 31% year-on-year, largely impacted by an explosive growth of 5G FWA in India (332% year-on-year) as well as the US (39%). In India, Reliance and Bharti Airtel are marching ahead with 5G FWA rollouts, capitalising on the huge potential of the enormous broadband hungry market.

We expect this trend to continue due to the fact that FWA networks are easier to scale after the initial investment, FWA broadband services being generally cheaper for consumers than the alternatives, easy to self-install, and being ‘good enough’ for streaming, remote work, and average household use, as well as the demand for connectivity in remote and underserved areas. Having said that, this applies primarily to the more advanced FWA, especially 5G based. We are also seeing a decline in subscriptions based on older FWA variants in some markets.

Satellite broadband subscribers saw a boost of 41.6% year-on-year, mainly due to the growing Starlink customer base that reached just over 6 million globally (5.7 million in the markets we track). The quarterly growth in Starlink subscriptions, however, was slower compared to Q1 2025 (9% versus 7% in our sample).

Figure 9 provides our estimated figures of Starlink subscribers in the largest 20 markets. The US continues to be the largest market with over 2.3 million subscribers but it grew only by about 2% in Q2 2025. Canada, Brazil, Argentina and Mexico are also in the top five, being large territories with vast remote areas where traditional broadband infrastructure is harder to install. Among the top 20 Starlink markets, Mexico and the Philippines saw the highest quarterly growth rates of 21% and 25% respectively.

Starlink’s prospective competitor Amazon’s Project Kuiper has been making progress in 2025 — shifting from prototypes to production satellites and securing multiple launch contracts. The project is still in the early stages - as of mid-October 2025, only 153 satellites have been launched, a small fraction of the 3,200 target.

According to the company, Project Kuiper will launch services in five markets by the end of Q1 2026 - Canada, France, Germany, the UK, and the US. However, to meet its licence requirements, the US Federal Communications Commission needs approximately half of the planned constellation of 3,200 satellites to be deployed by July 2026, a target that appears unlikely.

Concluding thoughts

Fixed (home) broadband subscribers continue to grow, mainly in the less saturated markets of the Globe. While fibre connections are seeing sustained demand, its growth in more mature broadband markets comes mainly from luring customers from other platforms (primarily copper and cable).

Around the world, we are witnessing the highest growth in advanced FWA and satellite broadband subscriptions, albeit from a much smaller base than FTTH/B. 5G FWA is particularly attractive because of its competitive prices, ease of self-install and broader availability in more demanding terrains and remote areas.

This analysis is based on our Global Broadband Statistics dataset.

Comments