Point Topic / INCA Annual Report 2026

- Veronica Speiser

- Mar 11

- 13 min read

Beyond disruptors: Altnets expanding future-proof infrastructure, driving competition in gigabit broadband

The Independent Networks Cooperative Association (INCA) asked Point Topic and Assembly Research to deliver the 2026 edition of its Annual Report. This study provides evidence of Altnet coverage, connections and concerns, as well as policy and regulation actions to support further investment and the creation of effective competition in the fibre market.

Below are excerpts from the report, which is available for download at the bottom of this article.

Annual report key metrics

Foreward

This is my second INCA Annual report and it’s been a pivotal year for the UK’s Telecoms Market and in particular the Independent Network Operators, the Altnets, as they have moved from disruptors to established players, shaping the market through investment, pace of delivery, and genuine customer choice. As the sector matures, the focus is shifting from build to take up and to sustainable economics with sharper competition, more disciplined capital and ongoing practical barriers that still affect speed and certainty.

In this environment policy and regulation will be decisive in securing a competitive investable gigabit market for the long term. Inca exists to represent that competitive network and the wider ecosystem that supports them, bringing evidence, convening practical solutions, and ensuring the Altnet perspective is heard by Ofcom, government, and stakeholders across the UK as the next phase of the Telecoms Access Review approaches. This report sets out the State of the Altnets and I thank INCA members and our partners for their support and engagement over the past year and in the creation of this report.

Paddy Paddison (CEO, INCA)

Key Messages

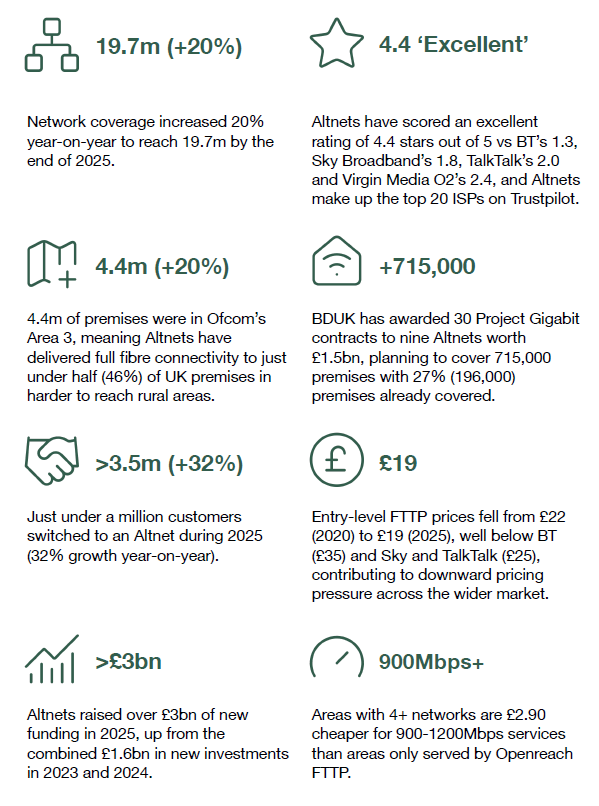

1. The UK’s independent (Altnet) operators increased their network coverage by 20% year-on-year to reach 19.7m premises at the end of 2025. Nearly 4.4m of these premises were in Ofcom's ‘Area 3’, meaning that Altnets have delivered full fibre connectivity to nearly half of all premises in hard-to-reach rural areas.

2. Over 850,000 customers switched to an Altnet during 2025, leading to more than 3.5m live fibre connections that are now delivered by independent broadband networks. This reflects 32% growth year-on-year, as well as an 18% take-up rate.

3. Altnets have delivered price certainty for end users by largely avoiding inflation-linked mid-contract rises, while strengthening price competition, particularly for entry-level fibre services. Altnets also outperform the largest retail ISPs on major consumer satisfaction rankings, maintaining strong levels of service quality and reputations for customer experience.

4. Revenues rose significantly in 2025, with four Altnets reporting to have achieved profitability for the first time. Despite a slowed pace of network rollout, the sector still invested over £2bn last year while attracting over £3bn in new external funding – some of which is expected to fuel future consolidation.

5. Altnets are most concerned about customer acquisition, reflecting a shift in priorities for Altnets (and their investors) from premises passed to actual connections. However, network deployment issues, such as PIA and wayleaves, remain top of mind, while the risk of overbuild by other Altnets has risen sharply within the set of challenges identified by the sector.

6. The outlook for the Altnet market will be shaped not only by commercial and operational factors, but also by regulatory and policy developments. Both Ofcom and the Government will continue to play a vital role in busting deployment barriers and enabling genuine competition in fibre networks, which will promote further investment, positive consumer outcomes and national-level growth.

Assessing the scale of the independent network sector

Table 1 below contains key metrics for the UK’s independent fixed networks from the end of 2023, with operators expanding their full fibre footprints by 35% on average over the three-year period, keeping pace with Openreach and increasing further market share from the three remaining major players1.

Premises passed and connected by fixed independent networks

At the end of 2025, the UK’s independent network operators are estimated to have passed 19.7m premises with their fixed broadband infrastructure. This is an increase of 3.3m year-on-year (YoY) compared to 3.5m in 2024. Altnets cover areas ranging from urban multi-dwelling units (MDUs), to new build homes to premises in remote and geographically challenging locations.

Yorkshire and the Humber has the largest Altnet coverage, with almost 60% of premises able to access an FTTP service from one or more alternative networks, followed by London (52%) and the West Midlands (51%) (see Figure 1). The North West, North East, East Midlands and South East are close behind, with around 48-49% of premises passed, while the East of England stands slightly lower at 46%. Coverage is more limited in the South West (40%) and the devolved nations, with Northern Ireland at 42%, Scotland at 37% and Wales at 26%.

Altnet take-up continues to increase on a YoY basis, albeit at a slower pace than initially anticipated by suppliers and investors. Live connections for independent operators stood at over 3.5m at the end of 2025, up from 2.7m or 32% YoY (see Figure 2). In terms of penetration, Altnets are seeing on average an 18% take-up rate, which is up two percentage points from the previous year. This indicates that, despite many Altnets cautiously slowing or pausing network build activity, a greater focus on marketing, customer acquisition and conversion is beginning to deliver incremental gains in subscriber take-up.

The ongoing reserved expansion of Altnet networks and gradual increase in take-up are contributing to a more competitive broadband market, placing gradual competitive pressure on incumbent providers and supporting improved choice and outcomes for consumers over time. Annual

Regional variation in Altnet coverage: Drivers and implications

Figure 4 below provides an overview of the regional distribution of Altnet-only versus no-Altnet network coverage at the end of 2025. For those regions lacking an Altnet presence, it is not indicative of a failed rollout model or low demand, but reflects a combination of economic viability, network build strategy and historical market conditions, rather than uneven consumer demand.

Although growth was widespread, its scale varied between local authorities, reflecting ongoing market pressures and a growing emphasis by suppliers on accelerating subscriber acquisition to support financial sustainability and investor confidence.

In many places, Altnets are the best and sometimes only option. There are millions of premises today that can only get an FTTP/B service thanks to the availability of alternative networks. Table 2 below provides a further breakdown of premises covered only by Altnet networks.

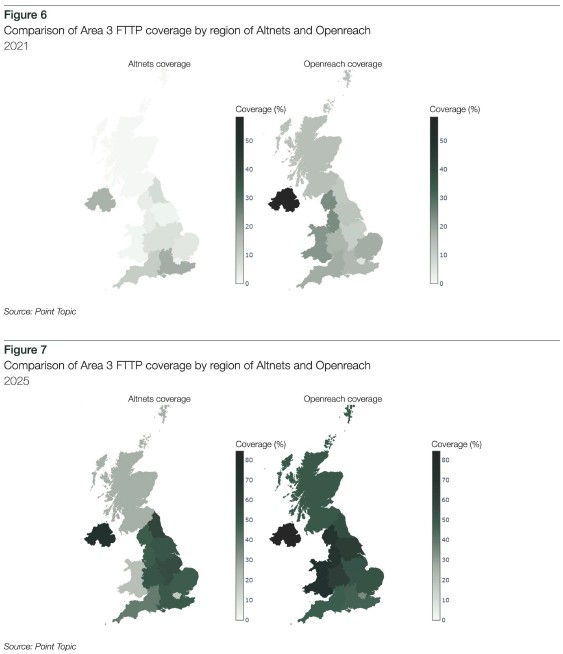

The Altnet effect: How independent networks have redefi ned Area 3

The Area 3 coverage maps indicate that this expansion has not been confi ned to isolated or niche deployments. Instead, there is clear evidence of geographic overlap and overbuild between Altnet and Openreach FTTP networks across many rural and semi-rural areas (see Figures 6 and 7). While competition remains uneven and many parts of Area 3 are still served by a single network, the growing presence of multiple fibre operators across a significant share of premises points to a more competitive landscape than originally anticipated.

Across all regions, Altnets covered 588,330 postcodes by the end of 2024, expanding to 684,664 postcodes by the end of 2025. This reflects a net increase of 96,334 postcodes, representing 16.37% overall growth.

While Area 3 is still (until March 2026) officially classified as non-competitive and HTR, both Openreach and Altnets are deploying in the same areas, which has created the competitive landscape Ofcom sought in its original WFTMR framework.

The data indicates that material network overbuild between Altnets and Openreach is now present across large parts of Ofcom’s Area 3 footprint and at the close of 2025, overbuild accounts for more than a third of Area 3 premises in several regions, including the North West (36%), North East (35%), West Midlands (35%), and Yorkshire and the Humber (34%), with similarly high levels in the East Midlands (29%) and East of England (27%) – see Figure 10.

Most notably, Northern Ireland stands out, with overbuild affecting 61% of Area 3 premises, suggesting particularly strong competitive overlap in rural and small-town markets. By contrast, London shows minimal relevance to Area 3 dynamics due to its small Area 3 footprint.

Pricing and performance

Altnets are delivering price certainty

Between 2020 and 2025, UK broadband pricing practices have seen clear divergences between large national providers and many Altnets. While the largest providers relied on inflation-linked mid-contract price increases (typically linked to CPI/RPI plus a fixed uplift), most Altnets avoided percentage-based in-contract rises altogether, instead offering fixed prices for the duration of the minimum term or, where increases applied, disclosing fixed amount (£) changes in advance.

Ofcom’s prohibition of inflation-linked price rises came into effect from 17 January 2025.2 The regulation mandated that ISPs must provide pricing transparency with any increases to be listed in pounds and pence, essentially formalising a pricing approach that many Altnets had already adopted.

Between 2020 and 2025, the UK full fibre or gigabit-capable broadband market has become materially more competitive, with Altnets maintaining an important role in shaping pricing dynamics, particularly in the entry-level segment (see Figures 11 and 12).

In 2025, Altnets’ entry-level pricing stood at £19, down from £22 in 2020, reinforcing their ability to offer lower-cost full fibre access than the major providers. Altnets retain a clear pricing advantage over BT, whose entry-level price has increased from £33 to £35, and remain below Sky (£25) and TalkTalk (£25).

Average pricing across the sector highlights a broader shift in the market. Altnets’ average price has remained broadly stable (£39 in 2020 versus £38 in 2025), suggesting that despite modest reductions at entry-level, the sector has maintained pricing strength overall, showing the growing demand for higher-speed full fibre packages.

The median pricing trends also reinforce this shift. BT and Virgin Media have moved from medians of £48 in 2020 to £35 and £27 respectively in 2025, indicating a repositioning of their broadband portfolios toward lower effective price points. Altnets’ median price has edged up slightly from £34 to £35, suggesting that their pricing is converging with the wider market at mid-range levels, even while they continue to offer relatively strong entry-level value. Sky has remained broadly stable on average pricing, but its median has fallen from £32 to £30, resulting from strong promotional activity, an increase in coverage through its agreement with CityFibre, and pricing competition in its core packages.

Altnets have played an important role in improving consumer outcomes by widening the range of available price points, particularly for low-cost fibre access, while simultaneously applying sustained competitive pressure on incumbents. The result is a more dynamic marketplace in which consumers benefit not only from lower entry pricing, but also from stronger price discipline among major providers and a broader range of competitively priced full fibre services.

The financial health of the industry

Investment flows

The telecoms sector was not immune to the challenging macroeconomic and political factors that have become commonplace since 2023. As has been widely reported, many Altnets have slowed their fibre network deployments to concentrate to a greater extent on increasing take-up and revenue, particularly in areas where they have a more established or mature presence. This shift is evident in operators' financial reporting, with Community Fibre stating around a 70% decrease in capex year-on-year.3

Nevertheless, this partial change in mindset and the restructuring or reorganisation activities of a minority of Altnets should not overshadow the sector’s continued investment, which has led to significant growth in fibre coverage in certain areas over the last twelve months. The £2bn of capex in 2025 demonstrates that network investment, including into rural and underserved parts of the country, continues to flow. For example, in January 2026, Grain made a number of separate rollout-related announcements, outlining plans to cover Sheffi eld in South Yorkshire and Goole in East Yorkshire, and stating that their deployment in Nuneaton in Warwickshire was now underway. These build on similar announcements Grain made regarding Wigan in Greater Manchester and Coalville in Leicestershire in December 2025.

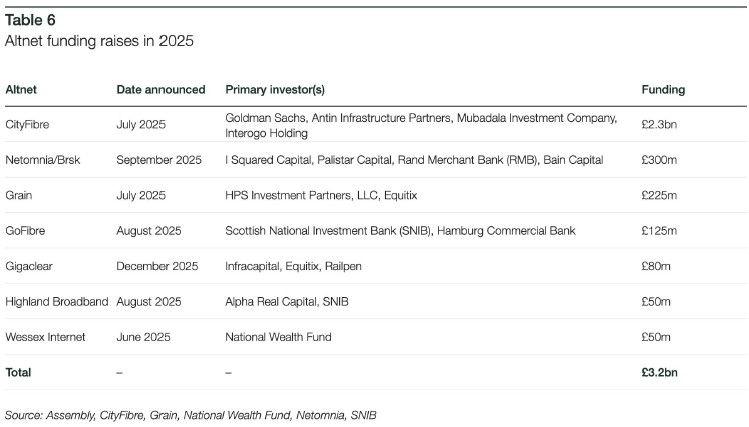

Meanwhile, external investment into the Altnet market recovered in 2025. In total, Altnets drew in over £3bn of new funding, a significant increase on the previous two years, which together only saw approximately £1.6bn of funding amid above-average interest rates and heightened investor caution (see Figure 14).

Although capital remains available, some operators have found it more challenging than others to access new funding from private investors, with certain institutions seemingly prioritising support for those Altnets perceived as being capable of challenging Openreach and Virgin Media O2 in the long-term. Gigabit IQ, an Altnet that mostly operates in Hampshire and Surrey, has taken an innovative approach, launching a crowdfunding campaign to raise £270,000 to support the future expansion of the business based on the principles of “safety, inclusion and trust”.

Financial performance

As Altnets look to prioritise adoption, some have reported hitting key milestones. In January 2026, Cumbria and Northern Ireland-based Fibrus announced that it had achieved 30% take-up across its fibre network, representing one of the strongest adoption rates in the industry and a customer base of more than 135,000. Similarly, in December 2025, Airband – a fibre and fixed wireless access (FWA) provider in Wales and South West England – announced it had reached 30,000 customers, an increase of around 11,000 from March 2024.

During 2025, Altnet financials reflected this progress in fibre adoption rates, with some seeing revenue uplifts of over 500%.5 Improving revenue performance represents the beginning of the take-up phase for the sector, while also resulting in certain operators reaching profitability in their earnings before interest, taxes, depreciation and amortisation (EBITDA) for the first time.

Consolidation trends

The prospect of mergers and acquisitions within the Altnet community continues to be one of the industry’s major talking points, even if consolidation is yet to proceed en masse. For the 2020-2025 period, we are aware of 20 successfully completed transactions (see Figure 15), including ‘in-family’ combinations (Netomnia/brsk, County Broadband/Truespeed), mergers (e.g. FullFibre/Zzoomm) and acquisitions, such as those spearheaded by CityFibre (Connexin, Fibre Nation, Lit Fibre) and Virgin Media O2/nexfi bre (Upp).

2025 saw six deals, including CityFibre’s acquisition of Hull-based Connexin. The mergers of FullFibre/Zzoomm and County Broadband/Truespeed were also significant, creating networks with over 600,000 and 177,000 premises passed, respectively.

The regulatory environment is expected to be conducive to further Altnet consolidation, with the combination of smaller, often more localised, providers unlikely to pose risks for competition. The Competition and Markets Authority (CMA) would not be expected to subject deals involving these players to any significant scrutiny. Review by the CMA is of course more likely in the context of deals between larger Altnets, such as the recently announced nexfi bre/Netomnia transaction.

Altnet risks and concerns

The INCA survey asked operators to rate how concerned they are about a range of factors related to challenges to their network deployment as well as their ability to offer services to, and acquire, customers. For 2026, Altnets identified customer acquisition as their most pressing concern, with three further issues ranked jointly in second place:

PIA availability and costs;

Street works and planning delays; and

Securing wayleaves and property access.

According to the survey, the Altnet market’s current primary concern is customer acquisition. With just under three-quarters of UK homes now able to access fibre broadband services6, widespread customer acquisition is the crucial next step to the Altnet market’s competitiveness with the established players. Encouraging the take-up of Altnet services has proved challenging though, with operators struggling to attract customers without a recognised and reliable brand while also facing public misunderstandings about differences between full and part-fibre options. This is an area where consolidation could be key, with the potential for a smaller number of larger providers to improve brand recognition and attractiveness for customers.

Access to finance and overbuild by Openreach went from being the sector’s top two concerns in 2024 to ranking joint eighth this year (see Table 8). However, overbuild by other Altnets (including Virgin Media O2/nexfi bre) ranked fifth – up from 15th in 2025, highlighting intensifying network-based competition across more of the UK.

In 2024, Altnets’ second largest concern was over the risks of Ofcom’s Telecoms Access Review (TAR), yet in 2025, these concerns have lessened significantly. Ofcom’s TAR proposals do little to suggest a revolution in its regulation of the market, with the regulator instead opting for a stable continuation of its current framework. However, Altnets remain concerned over certain TAR-related challenges, most notably regarding the risks of reduced regulation on SMP operators (i.e. Openreach and KCOM) as well as the prospect of higher PIA charges.

The scale of Altnet challenges

Although customer acquisition, PIA costs and planning issues have largely been perceived as the key concerns for the Altnet market in 2025, operators have not underestimated the scale of some of the other challenges they face. Altnets still see Openreach Equinox offers, overbuild by other Altnets and wholesale local access (WLA) pricing uncertainty as considerable issues, with 63% of survey respondents deeming these to be a challenge in some way – see Figure 16. Some challenges saw more division among Altnets though, with survey respondents equally split over whether access to finance and copper retirement are still a challenge in 2025. With regard to the access to finance issue, this divide makes sense given the wide disparities in investment between Altnets, with some operators still searching for funding while others have more definitively deprioritised further build-out for the immediate term.

Recommendations

Altnets are a key part of the connectivity jigsaw, helping to drive competition and consumer choice. Their future outlook will be shaped not only by a range of commercial and operational challenges, but also regulatory and policy factors. We have identified eight recommendations for Ofcom and DSIT to create the conditions conducive to continued investment and competitiveness, which would in turn help support delivery of the country’s connectivity and growth ambitions:

Maintain a commitment to a competitive fibre build: Ofcom’s approach to infrastructure and its regulatory decisions have facilitated a fibre build-out that has surpassed its own expectations. With the TAR statement imminent, Ofcom should continue to commit to a pro-investment, pro-competition strategy at the halfway point of its 10-year framework, broadly ensuring consistency and stability to maintain industry momentum;

Keep a watchful eye on wholesale price discounting: In light of offering a degree of freedom to Openreach over access pricing, the regulator should be vigilant in ensuring that price levels remain fair and reasonable, with any proposed promotions given appropriate scrutiny and prevented if they would negatively impact wholesale competition, for example by inducing loyalty;

Provide close oversight of duct and pole access: With PIA considered a foundational remedy, Ofcom is right to continue with unrestricted access to Openreach’s duct and pole network. Given the Government’s strategic steer, Ofcom should be prepared to be transparent and proactive in respect of any new reporting obligations regarding its calculation of cost-based charges, while closely monitoring that PIA is supplied according to the principle of no undue discrimination;

Prioritise planning reforms: Removing any further obstacles to fibre deployment should continue to be high on the Government’s agenda despite a number of successes by the Barrier Busting Task Force on this front. Taking utmost account of input from industry, DSIT should prioritise (even look to expedite) revisions to planning regulations to help sustain commercial fibre investment, which will underpin new flagship housing and data centre projects;

Consider the evidence of the impacts of flexi-permits: Adoption of a national flexi-permit system could improve the speed and efficiency of operators’ rollouts if local authority opposition can be overcome. The Government should carefully assess the evidence from recent pilot projects, collaborating with relevant stakeholders to explore how this initiative could be implemented with minimal administrative burdens or inconvenience to residents;

Ensure competitive MDU access: More straightforward access to MDUs would help accelerate access to fibre for tenants in block of flats; however, it should be pursued in a way that does not favour one provider over another. Dialogue and collaboration between stakeholders (e.g. Altnets, Openreach, property owners) will be key to help ensure working people are equipped with the tools for modern living without sacrificing consumer choice or competition;

Shift the focus to customer adoption: The Government has placed the onus on industry to promote fibre to consumers, while Ofcom’s work to date has also focused on boosting access rather than adoption. At this juncture, it is vital that the Government reflects on its role in encouraging the take-up of fibre services by consumers and businesses, potentially setting ‘north star’ targets, which may look similar to longstanding supply-side objectives; and

Explore a Supplier of Last Report (SoLR) process: While the UK has witnessed the emergence of scores of new fibre broadband providers, the Government should be mindful of the risk that competition in some parts of the country will not be sustainable, and that a number of smaller players could fail. By anticipating the worst-case scenario, an SoLR process would establish a safety net for affected customers and help industry ensure none are left without service.

1 Estimates are based on company reports, plus survey data supplemented by Point Topic research as outlined above, either reported to Point Topic by network operators or using our own estimates when actual numbers are unavailable.

2 Statement: Prohibiting inflation-linked price rises, Ofcom, 2024

3 See Annex 1

5 See Annex 1

6 Connected Nations update: Spring 2025, Ofcom, 2025

Comments