Q4 2025 Broadband Subscriber Trends: Growth Slows to 0.5% as China Reports Churn

- Jolanta Stanke

- Apr 27

- 7 min read

Summary

This report provides analysis of trends in global and regional broadband subscriptions, technology adoption, and growth rates in various markets in Q4 2025.

Global broadband subscribers surpassed 1.57 billion in Q4 2025, following a 0.46% growth. The modest uptick was partly due to the subscriber decline reported in China. In addition, compared to Q3 2025, broadband subscriptions[1] grew slower in 53 out of the 124 countries we track[2]. Jamaica was hit especially hard by the Hurricane Melissa. On the other hand, we restated up the figures for Ukraine, as the country’s regulator has now published a report, reflecting the last few years. Fortunately, broadband connections proved to be more resilient to the war than we had estimated.

Other key points:

The share of FTTH/B in the total fixed broadband subscriptions increased slightly and stood at 73.3%. Broadband connections based on other technologies saw their market shares shrink again, with an exception of satellite and fixed wireless access (FWA).

Year-on-year, FTTH/B connections grew by 6.4%. Satellite and FWA saw a much higher annual growth (30.2% and 36.8% respectively), though from a lower base.

Legacy copper subscriptions declined by 15.5% y-o-y, while FTTx lines (mainly VDSL) went down by 5%. Cable/HFC connections also fell by 3%.

5G FWA take-up accelerated further, especially in India and the US, with the former adding 1.6m and the latter over 1m subscribers in Q4 2025.

Quarter-on-quarter, cable and FTTx decline has accelerated, FTTH/B grew slower, while satellite and FWA growth gathered pace.

In Q4 2025, cable broadband subscriber numbers grew only in 16 out of 73 markets (in nine of them by less than 1%).

India remained at the top of the largest 20 fixed broadband markets with a 5.9% quarterly growth. China recorded a 0.6% decline.

[1] Whenever we refer to ‘broadband’ in this report, we mean fixed broadband. Also, ‘subscriptions’ and ‘connections’ are used interchangeably.

[2] It is possible there will be restatements in the coming quarter/s and single period data should be viewed in that light. Decline in some markets can be due to changes in methodology used by national regulatory authorities.

Global and regional trends in broadband subscriber growth

In Q4 2025, the global fixed broadband subscriber figure grew by 0.46%, exceeding 1.57 billion. The growth rate this quarter was the lowest in the last two years, mainly due to China reporting a decline in the country’s fixed broadband subscriptions as China Mobile’s customer base shrank (Figure 1 and Table 1). We will see next quarter if it was just a temporary blip, for example due to the clean-up of their figures, or whether it reflects already high household penetration in fast maturing market, as well as the impact of tariffs.

Table 1. Global broadband subscribers and quarterly growth rates. Source – Point Topic.

As a result of the Chinese figures, South and East Asia’s share of net adds in global fixed broadband subscribers was significantly lower this quarter, dropping from 67.2% in Q3 2025 to 5.7% in Q4 2025 (Table 2 and Figure 2). This has reduced the region’s market share slightly. Among other regions, only Western Europe saw its market share decline, while all the remaining regions experienced growth. In terms of net adds, Middle East and Africa and Latin America took the lion’s share, with 24.6% and 20% respectively.

Table 2. Share of fixed broadband subscribers and trends in net adds by region. Source – Point Topic.

Broadband penetration among population remains one of the important factors affecting growth rates, as illustrated by the Middle East and Africa (MEA), which remains at the bottom right corner of the penetration – growth chart (Figure 3), signifying the lowest penetration (9%) and the highest quarterly growth rate (2.1%). MEA retains a good growth potential, especially for FWA and satellite broadband connections. Some countries in the region are also heavily investing in FTTP.

At the other end of the spectrum, South and East Asia had the lowest quarterly growth (0.1%), with the decline in China having its effect.

Latin America and Asia-Pacific occupy the middle ground in terms of broadband penetration (20.4% and 18.3%) and quarterly growth (1.1% and 0.9% respectively). Along with its higher broadband penetration (29.2%), Eastern Europe also recorded a modest 1% quarterly increase in broadband connections. We should note that we restated up the figures for Ukraine, as the country’s regulator has now published a report, reflecting the last few years, including the impact of the war on broadband subscriptions. Fortunately, it was not as devastating as we had estimated.

North America and Western Europe are both at the top by penetration, which means more sluggish growth. North America fared slightly better with 0.6%, where FWA had a particularly strong quarter in the US. Western Europe remained in the top left corner of the chart, with high penetration (42.5%) accompanied by modest growth (0.3%), caused by sub-1% rise in broadband subscribers in most markets and a decline in some.

Among the largest twenty broadband markets, all except China saw fixed broadband subscriber increase in Q4 2025 (Figure 4). For several quarters now India has been at the top of this cohort (5.9% q-o-q), continuing to show huge growth potential due to the low fixed broadband penetration (18% of households) and the fast growing economy. In Q4 2025, India recorded a further dramatic increase in 5G FWA connections (+16.9% quarter-on-quarter).

The developing economies of Egypt, Indonesia, Argentina and Vietnam saw 2%+ quarterly growth in fixed broadband subscribers. Overall, compared to Q3 2025, the growth was slower in 13 markets.

Technology trends in broadband subscriber growth

Once again, the market share of fibre based broadband subscriptions (FTTH/B) has expanded slightly – quarter-on-quarter it went up by 0.26% and stood at 73.32%. Broadband connections based on cable, copper and FTTx technologies saw their market shares shrink further. Satellite and wireless (FWA) broadband connections expanded their market shares to 0.54% and 3.46% respectively. (While their market shares are still in low figures, the latter two technologies are showing the highest growth, on which more later).

Table 3. Changes in broadband technology market shares. Source – Point Topic.

Among the markets with at least 0.5 million fibre broadband connections, we recorded the highest FTTH/B growth rates in Egypt (16%), Algeria (14.2%), Belgium (12.8%), Greece (11.9%), and Chile (11.7%) (Figure 5). Along with young / low broadband penetration markets, this ranking once again contains mature broadband markets of Belgium, Greece, and the UK. While having high overall broadband penetration, these countries were relatively late in focusing on full fibre, thus experiencing high growth rates from a lower base.

Globally, healthy quarterly FTTH/B growth rates were spread around the world, with the less advanced economies and more youthful fibre markets generally exhibiting higher growth (Figure 6).

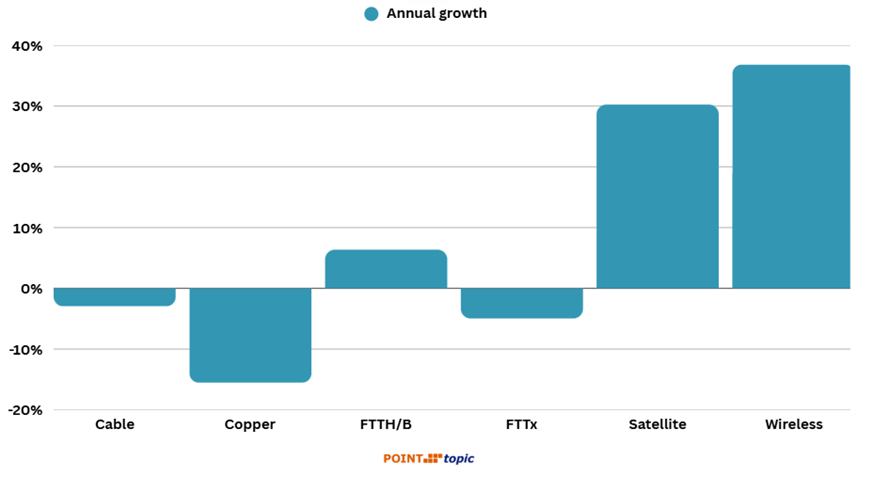

While FTTH/B was the only wired broadband platform seeing subscriber increase in 2025, the growth of wireless and satellite technologies was significantly higher (admittedly, from a lower base). In 12 months to the end of 2025, FTTH/B lines grew by 6.4%, while satellite and wireless (mainly 5G FWA) connections increased by 30.2% and 36.8% respectively. The number of copper (DSL) lines saw another decline (-15.5%), while FTTx lines dropped by 5% and cable (HFC) broadband subscriber number fell by 3% (Figure 7).

Quarter-on-quarter, cable and FTTx decline has accelerated, FTTH/B grew slower, while satellite and FWA growth gathered pace (Figure 8). Legacy copper market share is already tiny at 3.6%, so its decline has slowed down to some extent, with households unreachable or unconvinced by more advanced technologies holding on to it.

While the decline in legacy copper and part copper is not surprising, cable/HFC also appears to be on the way out. In Q4 2025, cable broadband subscriber numbers grew only in 16 out of 73 markets (in nine of them by less than 1%). The US, the world’s largest cable market, saw a further drop in cable broadband subscribers (-0.7%), with Charter losing more than 100K and Comcast nearly 200K.

Competition from fibre and 5G FWA home broadband offerings from T-Mobile, Verizon and AT&T have exploded, with their customer numbers jumping year-on-year by 32%, 25% and 102% respectively. (T-Mobile had also entered the full fibre market and was approaching 1m fibre subscribers in Q4 2025). Aiming to increase its FWA subscribers to 8-9 million by 2028 and expand FWA availability to 90 million households, in Q4 2025 Verizon announced the acquisition of Starry, which serves 100k MDU customers in five markets: Boston, New York, Los Angeles, Denver, and Washington, D.C.

India is another sizeable 5G FWA market, where connections jumped by 113% year-on-year, with both Reliance and Bharti Airtel continuing to invest aggressively in their 5G FWA rollouts.

We expect this trend to continue as FWA based services are generally cheaper than the alternatives, and are increasingly sufficient for streaming, remote work, and other uses, as well as being a more feasible option for deployment in remote and underserved areas.

Satellite broadband subscribers grew by 30.2% year-on-year (8.6% quarter-on-quarter), mainly due to the growing Starlink customer base that reached 6.8 million (in the markets we track). The largest markets remain the US (2.3m), Brazil (0.6m), Canada (0.6m), and Argentina (0.4m) (our estimates).

The most important long-term challenger to Starlink is Amazon’s Project Kuiper, now Amazon Leo. But Amazon is not yet the main competitor in the market, because its service is only expected to be launched in 2026 after an enterprise preview began in late 2025. Amazon does have serious strengths: a licensed constellation of more than 3,000 satellites, deep capital, AWS integration, and several named enterprise customers and partners. Still, it remains far behind Starlink in deployed scale and live customer base.

Our customers subscribing to the Global Broadband Statistics product can access the complete dataset containing the data at the country, operator and technology level.

Comments