FTTP broadband subscribers to reach 1.12bn in top markets by 2030

- Jolanta Stanke

- Jun 18, 2024

- 9 min read

We have completed our latest forecasts for fixed broadband subscribers by technology. They are based on our Global Broadband Subscriber figures for up to Q4 2023. For full methodology of the forecasts, see the final section of this analysis. The complete dataset referred to in this analysis is available to our Global Broadband Statistics (GBS) and European Broadband Observatory (EBO) subscribers.

By 2030 we are projecting a total of 1.39 billion subscribers to a fixed broadband connection in the 29 largest broadband markets in the world. Full fibre (FTTP) is already dominating most of the markets and it will be the preferred option for most consumers, where it is available.

Split by technology we estimate that by 2030 there will be 1.12 billion FTTP, 149 million cable, 79 million FTTX, 16 million FWA[1] and only 28 million DSL lines in these markets.

Between 2023 and 2030 we project a 15% growth in total fixed broadband subscribers in the top 29 markets. The growth will come mainly from FTTP – although the increase in the total fibre lines will be lower than that in Fixed Wireless Access lines – 25% and 61% respectively, the sheer number of already existing and new FTTP connections will drive the total growth.

Cable is a term we used as a proxy for those legacy operators (e.g. VMO2, Charter, Comcast) that still have significant networks based on coaxial cable, mainly DOCSIS3 and 3.1. We forecast some decline (-6%) in cable broadband lines by the end of the decade as these networks are being replaced with full fibre. The new generation DOCSIS4, which is in development, will match the capabilities of FTTH with XGPON, so markets with established cable networks will see a slight growth or stable take-up figures for ‘cable’ broadband lines.

FTTX (where fibre is present in the local loop with copper, mainly fibre to the cabinet) will decline over the next seven years (-19%). Some modest growth from new subscribers will remain in a few markets where legacy infrastructure is still wide-spread. Also, it will remain a cheaper option even where other technologies are available as it still offers enough bandwidth for some users.

DSL will see the largest decline at -44%. However, while being a slower and less reliable solution, it can provide enough bandwidth at a low price to some single or older households that are reluctant to upgrade. Besides, some of them will not have a choice of other technologies, especially in certain regions and markets.

Regional breakdown

In terms of fixed broadband penetration regardless of platform, 4 out of 5 regions will see it rise to more than 70% by 2030. Africa, where fixed infrastructure is still quite limited, will be approaching 60% and will record the largest increase between 2023 and 2030 (+18%), driven by Egypt and Algeria. Europe will see it above 90%, with many markets already saturated or almost there.

Full fibre will drive broadband subscriber growth in most markets. It is already the market leader in 2 out of 5 regions (Asia and Europe) and will become the dominant technology in the Americas by 2025. In Africa, full fibre deployment is in the very early stages, so copper connections will still outstrip fibre by a large degree.

Asia will dominate in terms of total numbers and penetration, with China, India, Indonesia and others enjoying large populations and abundant potential new subscribers, although mobile technologies remain an important means of broadband access in these markets.

Mainly due to China’s investment in fibre, this technology will dominate fixed broadband connectivity in this region, with other technologies paling in comparison to it.

Europe will see stagnation in cable broadband connections and decline of copper (DSL more sharply than FTTX), while we expect full fibre take-up to accelerate, as network coverage and consumer choice expand further.

Our analysis of Oceania is based on Australia only[2]. Some of the reporting from Australia is unclear when it comes to ‘full fibre’ with FTTN and FTTC included in the operator totals. At the country level, FTTP has seen its market share of the total lines decreasing at the expense of FTTC and FTTN but again the reporting is limited. As a result, we have included Australia’s FTTP in the broader FTTX category, so increasing FTTX penetration in the region will mean higher speeds for more consumers but not necessarily ‘full’ fibre. Meanwhile, cable (HFC) is being phased out by the country’s operators.

Asia is expected to have the highest regional FTTP penetration by 2030 with nearly 67% of households and businesses subscribing to a full fibre service. As mentioned earlier, China is the main driver but rapid progress in terms of fibre deployment is also being made in other markets. Having said that, some countries in the region are still relying on legacy infrastructure.

Europe will follow Asia closely, with nearly 63% FTTP penetration, with a number of mature fibre markets already approaching saturation (France, Portugal, Spain), while others are catching up at speed.

In the Americas, markets like the US, Canada and Argentina will have high take-up of ultrafast fixed broadband but the strength of the ‘cable’ sector means it will see a slower decline compared to other regions. In the US, for example, we project that cable penetration will remain higher than that of FTTP. In turn, this means we project a relatively lower FTTP penetration in the region in 2030 - at 51%.

In Africa, as Egypt and Algeria are investing in full fibre, FTTP penetration will grow to 14%.

In comparison, in 2023, there was widespread adoption of fixed broadband but FTTP penetration stood at under 40% in all regions except Asia (see the earlier note on Oceania).

Country view

All largest markets will see higher fixed broadband penetration by the end of the decade, with China, India, United States and Brazil having the highest numbers of connections.

A word of caution on China, however. In the official Chinese data, while the reporting seems very clear and there are some very useful looking metrics, we have difficulty reconciling the total number of broadband lines with the estimated number of ‘households’ and business premises.

China has a total population of 1.4 billion and approximately 525 million households (data from 2021) and the report above quotes 590 million fixed line subscribers (Dec 2022).

Again, from the report (pg. 15) you would expect the number of households with a fixed line to be of the order of 390 to 400 million (75.6% of 525 million) assuming one line maximum per household and conflating adoption by netizens with household lines. This would mean 130+ million fixed line subscriptions would be ‘business’ or non-residential.

Nonetheless, China Is the largest broadband market today and will remain so at the end of the decade.

In terms of fixed broadband penetration, we project India to have the lowest percentage of premises with a connection, at 33% (up from 11% in 2023) and the most headroom available while France and South Korea will approach 100%.

We expect penetration above 90% in 16 out of the 29 markets (mainly developed or fast-growing economies), so headroom and potential for signing up new customers will shrink in these countries. Broadband providers in these markets will have to convert existing customers to higher bandwidth and more advanced technologies.

‘Full’ fibre – the future is bright

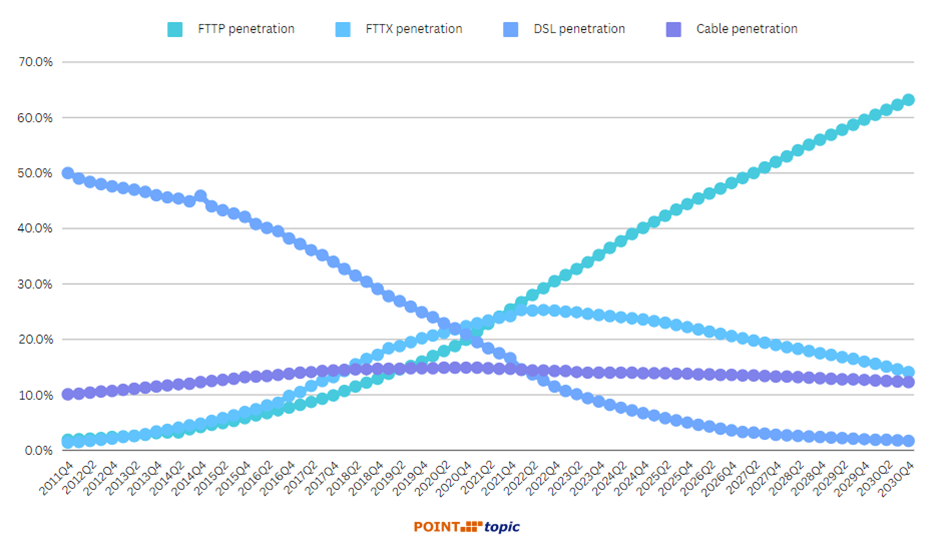

We have been tracking FTTP around the world since the start of 2010 and this allowed us to produce more accurate projections with good timelines to train models on. As we can see from analysis so far, FTTP will become the dominant platform at the expense of the other technologies.

Looking at specific markets, we can see gentle curves in many of the mature markets in Asia (Japan, Korea, Taiwan) where FTTP has been available for some time. In Turkey, legacy infrastructure is still widely used, while India and Indonesia will be two of the potentially most active markets in the second half of the decade.

In Europe, the likes of Portugal and Spain are approaching maturity in terms of fibre broadband connections. In most markets, however, there is still a lot of potential to migrate subscribers from other platforms but less headroom in terms of the overall new subscribers as fixed broadband penetration in the region is already high. At the same time, countries like Germany, Belgium and Italy still have to make significant progress to bring FTTP coverage to the majority of their populations, with the current fibre availability below the EU average.

The Americas, dominated by the US and Brazil in terms of the scale of FTTP connections, will see accelerating growth in the second half of the decade. While the cable market will restrict numbers of FTTP subscribers in the US and Canada, there are still plenty of customers to target. In South America, the potential is even greater, with Mexico, Argentina and Colombia joining Brazil in this respect.

Legacy networks still have life in them

Slower FTTP adoption in some markets can be partly due to the availability of alternative technologies. In particular FTTX, which is a deeply entrenched and mature technology in certain markets, is a barrier as consumers are difficult to convert when they have an adequate service.

Sizeable legacy infrastructure in the UK, Italy, Germany and Turkey is responsible for slower take-up of FTTP and slower deployment as operators need a longer timeframe to get a return on investment. FTTX can meet the needs of a significant number of subscribers, who are quite content with 40-80Mbps speeds and and even 10Mbps on xDSL in some cases.

So, while traffic hungry users are migrating to full fibre, the less demanding consumers are staying on FTTX or xDSL. While copper will gradually disappear, even in those markets where ‘copper switch off’ is being planned, there will still be legacy subscriptions for a while.

Concluding thoughts

By the end of the decade, most of the largest markets will see higher fixed broadband penetration and increasing dominance of full fibre. However, legacy networks still have a part to play in the markets and segments where users are happy with lower bandwidth and / or where full fibre and other ultrafast options are not available. Furthermore, in developing countries especially, mobile networks offer strong competition, whether due to their attractiveness to younger demographics, better coverage or price. Satellite and fixed wireless are also gaining momentum in some markets, where fixed solutions are not feasible.

There is significant growth to come in the ‘youthful’ markets with low fixed broadband penetration, with plenty of consumers in India, Indonesia and other fast-growing economies hungry for the advantages offered by fixed broadband and full fibre in particular. This is also true for more mature markets where full fibre coverage is far from complete. Here governments have a role to play, and those that appreciate the advantages of high bandwidth economies, will encourage investment. Whether they will favour incumbent operators or open competition, will vary across the countries.

On the other hand, in the markets with high fixed broadband penetration and already high FTTP coverage, fibre broadband providers still have consumers to fight for, although they will have to convince some of them to migrate from legacy technologies which might be seen as ‘good enough’. It should become easier with the passage of time, as experience in many markets suggests that the longer a fibre network has been around, the higher the take-up of services tends to be.

The complete dataset referred to in this analysis is available to our Global Broadband Statistics (GBS) and European Broadband Observatory (EBO) subscribers.

Appendix: sources and methodology

We have forecast fixed broadband subscribers by technology in the top 29 global markets[3] for the period ending Q4 2030. The aim of the forecast is to predict which broadband technologies will come to dominate in the largest broadband markets, perhaps at the expense of other fixed or mobile technologies.

The main input to the forecast is Point Topic’s Global Broadband Subscriber (GBS) data, collected and estimated quarterly at the operator and country level. For the purposes of this forecast we used the GBS data covering the period between Q4 2011 and Q4 2023. Another input was operator and regulator announcements about broadband network deployment plans and targets for the next 5-10 years.

The initial stage of forecasting was completed using one of the two models:

Logarithmic function: ln_x = np.log(x)

Logistic function: L / (1 + np.exp(-k*(x-x0)))

For each country and technology combination we selected one of the models that best fit the existing data and trends in broadband subscriber figures.

In the next stage, the model outputs were adjusted, where necessary, taking into account network deployment announcements and the number of premises in a country (upper limit).

The forecast number premises was based on the UN population estimates and projections[4] and UN Household Size and Composition data[5].

Technologies covered and caveats

Our forecast covers the main fixed broadband technologies:

DSL (mainly ADSL but including VDSL in some cases)

Cable (including Docsis3.0 and Docsis 3.1)

FTTP (FTTH)

FTTX (mainly VDSL, but also other variants of fibre-to-the-X)

FWA (some countries only)

The variations on which technology group includes VDSL (DSL or FTTx) depend on the reporting be regulators/ operators across the countries.

We forecast FWA figures only in the countries where they are significant.

For more details and caveats consult the following table.

Table 1. Countries and technologies covered in the forecast

Country | Technologies | Notes and caveats |

Algeria | DSL, FTTP |

|

Argentina | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

Australia | DSL, Cable, FTTx | FTTx includes some FTTB, FTTP and FTTC |

Belgium | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

Brazil | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

Canada | DSL, Cable, FTTP, FTTx, FWA | FTTx = VDSL |

China | FTTP | DSL, VDSL and cable figures are relatively small |

Colombia | DSL, Cable, FTTP, FTTx | FTTx = VDSL + FTTx |

Egypt | DSL, FTTP | DSL includes VDSL |

France | DSL, Cable, FTTP | DSL includes VDSL |

Germany | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

India | DSL, Cable, FTTP, FTTx | FTTx includes FTTx+LAN and FTTx |

Indonesia | DSL, Cable, FTTP | FTTP includes some FTTB |

Italy | DSL, FTTP, FTTx, FWA | FTTx = VDSL, no cable in Italy |

Japan | DSL, Cable, FTTP |

|

Korea, Republic of | DSL, Cable, FTTP, FTTx | FTTx = FTTB+LAN + FTTx+LAN |

Mexico | DSL, Cable, FTTP |

|

Netherlands | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

Philippines | DSL, FTTP, FWA |

|

Poland | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

Portugal | DSL, Cable, FTTP |

|

Romania | DSL, Cable, FTTP | DSL includes VDSL |

Spain | DSL, Cable, FTTP | DSL includes VDSL |

Sweden | DSL, Cable, FTTP | DSL includes VDSL |

Taiwan | DSL, Cable, FTTP | DSL includes VDSL |

Thailand | DSL, Cable, FTTP | DSL includes VDSL and ‘unknown’ |

Turkey | DSL, Cable, FTTP, FTTx | FTTx = VDSL |

UK | DSL, Cable, FTTP, FTTx | FTTP includes some FTTB, FTTx = VDSL + FTTx + G.fast |

USA | DSL, Cable, FTTP, FTTx, FWA | FTTx = VDSL |

Vietnam | DSL, Cable, FTTP | DSL includes VDSL |

This report is based on our Global Broadband Subscriber figures for up to Q4 2023. For full methodology of the forecasts, see the final section of this analysis. The complete dataset referred to in this analysis is available to our Global Broadband Statistics (GBS) and European Broadband Observatory (EBO) subscribers.

[1] We projected FWA figures only in the countries where they are significant and we had reliable data (Canada, Italy and the US). A more in-depth analysis of this technology, including 5G FWA, is to follow in our future forecasts.

[2] It is the only market from the region that falls within the 29 largest broadband markets.

[3] Excluding Russia, Ukraine and Iran due to the difficulty of forecasting for these countries at the moment.

Comments